.png?width=600&height=314&name=Resources%20Thumbnails%20(46).png)

Taxes can be intimidating for many business owners. A simple Google™ search for “small business tax tips” brings up many results that may only apply to a specific industry or type of business. However, there are six strategies that all business owners can implement to make sure they are reducing their tax costs as much as possible.

→ Watch Now: Election Special: Tax & Market Update

1. Choose the Appropriate Tax Structure

Business owners have several options to choose from when deciding what form of business entity to establish. The type of structure you chose determines the type of income tax return required for filing and impacts how much you owe.

There are many options for how a business can be tax structured, but which one is best? The answer depends on several things, including your business type and exit strategy. Your organization structure is especially important when you plan to sell your business. For example, if your succession plan involves private equity, a C-corporation may be the best option.

For many business owners, the most effective structure is a flow-through entity such as a sole proprietorship, partnership, limited liability company, or S-corporations, because there is only one level of taxation. Additionally, there is the qualified business income deduction which can give business owners up to a 20% deduction on their flow-through business income.

2. Separate Personal Finances from the Business

CEO and Founder of Oak Street Funding, Rick Dennen, describes an example of a common tax strategy that seems efficient in the short term but can be detrimental in the future.

“We see business owners run every personal expense through their business, so they in effect have no income tax to pay at the corporate level. However, when they decide to borrow money, the books show that they aren’t making any money, and this makes lenders more hesitant to work with them.”

Separating personal expenses from the business is especially important in mergers and acquisitions. Steve Blake, former Principal at Somerset CPAs and Advisors, explains how this approach is harmful for a seller’s business valuation. “If you’re running personal expenses through your books when the buyer takes a look at your business health, it will negatively impact the price they are willing to pay for your business.”

3. Take Distributions Instead of a Salary

Finding the balance of how much salary to take as a business owner can be difficult. There are IRS fines for underpaying yourself, but overpaying may mean you are overtaxed. Instead of taking a large salary, business owners can take payments as distributions to save on taxes. According to Jane Saxon, who was Principal at Somerset CPAs and Advisors, business owners should look at their role in the business as an employee and as an investor. For example, consider how much you would pay a general manager for your business and take that amount as salary. Then, your reward as an investor comes out as distributions, which is completely separate. Reclassifying your salary payments as distributions typically means they are payroll-tax free.

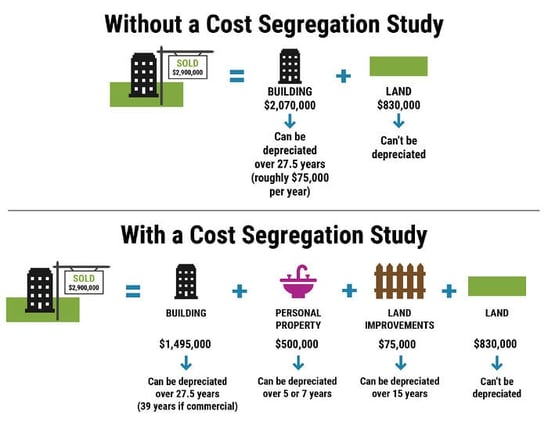

4. Participate in a Cost Segregation Study

Another great resource for business owners to save on taxes is a cost segregation study. A cost segregation study identifies and reclassifies property assets to shorten the depreciation time, which reduces current income tax obligations. Even if you purchased property a long time ago, a cost segregation study can reduce your taxes. The image below shows an example of a cost segregation study and its benefits.

5. Contribute to a Donor-Advised Fund

Charitably inclined business owners have options for making donations to increase their tax benefits. One of those options is a donor-advised fund. The donor-advised fund allows you to manage the deductions and stack those donations into the years when you have a higher income. The charity receives the same amount of funds, but when you disperse those funds is based on when you would receive the most tax benefit.

6. Find partners who understand your business

A key strategy to implementing the best tax practices for your business is finding consultants who are very familiar with your industry. The right consultants will help ensure you are taking advantage of all the tax provisions that may apply to you. This is possible only when your partners have a deep knowledge of your type of company.

Conclusion

With these six strategies, getting the most out of your tax plan is within reach. For more information, contact CBIZ or Oak Street Funding to amplify your tax savings and business growth.

Disclaimer: Please note, Oak Street Funding does not provide legal or tax advice. This blog is for informational purposes only. It is not a statement of fact or recommendation, does not constitute an offer for a loan, professional or legal or tax advice or legal opinion and should not be used as a substitute for obtaining valuation services or professional, legal or tax advice.

/Resources%20Thumbnails%20(47).png)

/Resources%20Thumbnails%20(20).png)