January 23, 2023 •Oak Street Funding

.png?width=600&height=314&name=Resources%20Thumbnails%20(43).png)

Why should a business owner who’s happy in their work give any thought to a tax-efficient exit strategy? Even if you have no plans to retire in the foreseeable future, thinking about the inevitable time when you’ll leave the business will give you more options to choose from, along with a framework for making important decisions about the business.

For most owners, their business represents their largest financial asset and is at the center of their ability to enjoy the retirement lifestyle they envision or provide long-term financial support to their dependents. Too many owners see exit strategies as a proverbial tin can they can keep kicking down the road until they believe they’re “ready” to step aside.

Unfortunately, waiting until then may limit their opportunities to sell or impact the optimization of the cash available to them post tax if not previously thought through. The pandemic has taught many of us that unforeseen health problems may make it impossible for them to play an active role in determining the exit. Either way, the tax consequences of failing to plan can be significant.

→ Watch Now: Tax & Market Implications Post-Election

Taxes and the exit

By beginning exit planning long before you actually plan to exit, you and your financial advisors can structure an approach that will maximize the value you’re allowed to keep, reduce the taxes you may owe, and minimize the tax burden for the eventual new owners.

If you’re already thinking of passing ownership to family members or trusted employees, careful planning today will inform the decisions you’ll have to make along the way to make the eventual transaction a win-win for both you and the eventual owners.

Additionally, if your goal is to sell the business to a third party at some point in the future, your exit strategy should offer ways to protect the value of the business assets and consider how to minimize taxes on the eventual sale. Doing that now is important because if you wait to start planning until someone makes an offer, you’ll have fewer options.

#1: The Gift Tax Exclusion

Even if you’re familiar with the annual gift tax exclusion, you may not have thought of it as part of an exit strategy, but it can provide an effective way to limit taxes on the ownership transfer of a closely held business.

The gift tax exclusion allows one individual or a married couple to transfer cash or other assets to another individual up to a certain limit, tax-free. For tax year 2023, the limit has increased to $17,000 for an individual and $34,000 for a married couple. Business owners can use the gift tax exclusion as a strategy for gradually handing ownership over to their children.

Suppose a husband and wife owned a business worth just over $500,000. They intend to pass ownership of the business along to their three adult daughters. Each year, they gift each of the daughters a share of the business worth the maximum tax-free contribution, so in 2023, each daughter will receive $34,000, for a total of $102,000. Over the course of about five years, the couple can pass the entire value along without a tax liability.

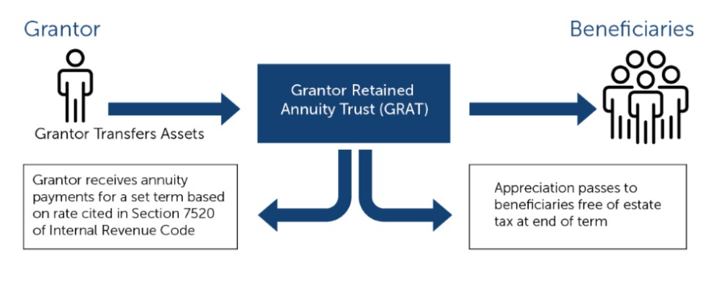

#2: The GRAT

Another tax-efficient exit strategy involves the use of what’s known as the grantor retained annuity trust (GRAT). This type of trust allows an owner to move their interest in the business out of their personal estate and into the trust, often at a low valuation. As the business grows, that increase in value happens within the trust.

Later, when the trust ends, the beneficiaries will take ownership of the business without being subject to estate taxes. There is a downside if the owner dies before the trust ends. In that event, ownership will return to the owner's estate, and the company's full value will be subject to estate taxes.

#3: The Family Limited Partnership

If an owner plans to pass ownership of the business to children or other members of the family, a family limited partnership (FLP) can help reduce the associated gift and estate tax liability. The owner creates an FLP and moves the business assets into it. In return, the owner maintains 99 percent interest in the limited partnership. The owner also keeps a one percent general partnership interest, allowing them to continue to maintain control over the business.

As time passes, the owner gradually gifts shares in the FLP to their children. Those shares have a lower value because they do not carry any control of the company, so the owner can pass along more of the business each year without incurring gift taxes. When the owner is ready, they transfer the general partnership interest to the children, giving them control of the FLP assets.

#4: Is an ESOP right for you?

If you’re considering an exit that involves transferring ownership to your employees or multiple family members, an employee stock ownership plan (ESOP) may offer both a practical blueprint and a tax-efficient exit strategy. A carefully structured ESOP can give a business owner a long-term plan for exiting the company, provide a way to tap into some of the company’s value, and allow time for the new owners to gain the experience and confidence to ensure the business will be sustainable for the foreseeable future.

ESOPs are only available to corporations, so a business that’s currently an LLC, partnership, or sole proprietorship will need to change its form of entity. Legally, ESOPs typically function as a form of qualified retirement plan that invests in your company’s shares of stock (and they come with specific legal requirements, restrictions, and rules). Once the participants are fully vested, they can receive either stock or its value in cash.

→ Working Capital Loans and Lines of Credit

Why ESOPs are tax-efficient exit strategies

Contributions made by the company to acquire the owner’s shares of stock are generally tax-deductible. In fact, a company could conceivably use debt to finance the purchase of shares and deduct not only the amount paid but the loan interest, too. For Subchapter S corporations, the portion of income belonging to shares held by the ESOP isn't subject to federal (and often state) taxes.

A key advantage of an ESOP is that it gives the current owner a way to gradually transition ownership and withdraw money over time, as opposed to receiving the full value in a single lump sum. In some situations, the funds can be reinvested to reduce capital gains tax liability. The owner can continue to lead the management team, even after the owner’s share shrinks to a minority interest. An ESOP can also be coordinated effectively with an owner’s estate plan.

Conclusion

No matter the exit strategy you choose, taking steps today to plan for your exit will allow you more options for the most tax-efficient exit.

Disclaimer: Please note, Oak Street Funding does not provide legal or tax advice. This blog is for informational purposes only. It is not a statement of fact or recommendation, does not constitute an offer for a loan, professional or legal or tax advice or legal opinion and should not be used as a substitute for obtaining valuation services or professional, legal or tax advice.

/Resources%20Thumbnails%20(75).png?width=600&height=314&name=Resources%20Thumbnails%20(75).png)